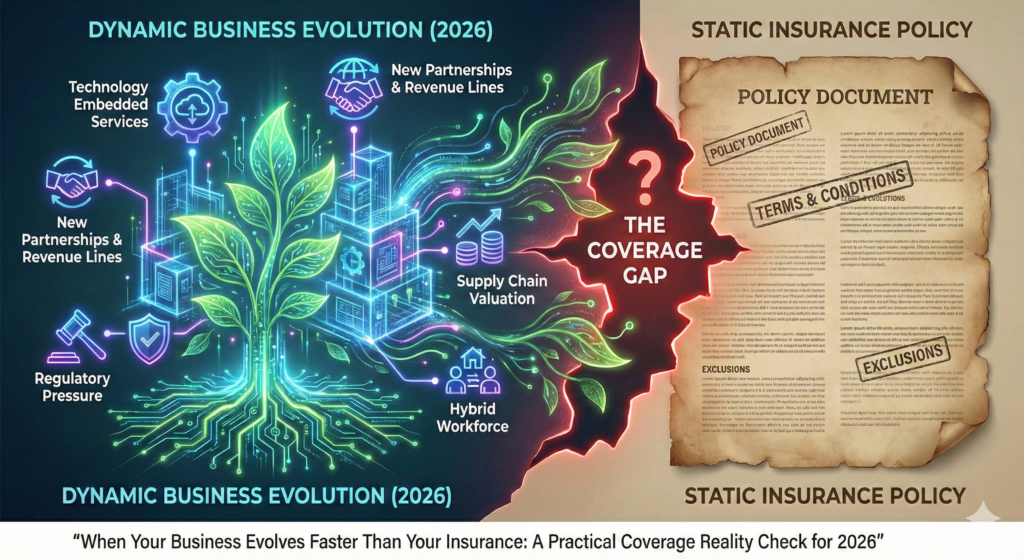

A business is a living organism. Your insurance policies are static documents.

That gap—between how you operate today and how you were described when coverage was placed—doesn’t show up when things are calm. It shows up during a claim, when someone asks: “Is this even covered?”

In 2026, that gap is widening for a lot of organizations because operations are changing fast:

- More technology embedded into services

- New revenue lines and partnerships

- Heavier regulatory and litigation pressure

- Supply chain-driven valuation swings

- Hybrid workforces and outsourced functions

A prevention-first risk program includes a coverage reality check—not a sales pitch, not a policy deep-dive—just a structured way to make sure your protection matches your current reality.

How do “silent coverage gaps” happen?

Usually in one of three ways:

Your services have expanded, but the definitions didn’t

If the “professional services” description doesn’t match what you get paid to do, you may have uncovered work—especially as businesses add advisory, tech-enabled, or hybrid services.

Your risk has shifted, but exclusions stayed the same

Standard forms often rely on broad exclusions that become dangerous when you cross into ownership stakes in projects, technology platforms you provide, or patient-facing services that now include digital delivery.

Your loss severity environment changed

Even if operations haven’t changed, claim outcomes have. Social inflation and nuclear verdicts can put pressure on liability programs—especially in project-driven industries where third-party injury and property damage claims can become limit-testing events.

What should a coverage reality check look for?

Think of this like a pressure test—where a claim is most likely to stress the program.

For leadership liability (D&O): what are the pressure points?

Leadership liability risk often lives in governance details. A practical check asks:

- If we’re sued by investors, partners, or regulators, do we have real defense protection?

- Are there carve-outs that create surprises after a cyber event?

- If the company faces financial distress, do directors have personal asset protection layers?

- How are we using AI – and do we have the appropriate governance policies in place?

You’re not trying to memorize technical language. You’re trying to understand what would happen in the first 72 hours of a serious leadership claim.

For professional liability (E&O): what questions uncover hidden gaps?

A practical E&O check comes down to three questions:

Does the policy describe what we actually do today?

If your operations include new “verbs” (design, manage, consult, integrate, maintain, deploy), the policy should reflect that reality.

If we catch an error mid-project, can we fix it without waiting to be sued?

Many policies respond when there’s a claim for damages. Some businesses benefit from a structure that supports corrective action early to prevent bigger losses and schedule disasters.

Are we wearing multiple hats?

Ownership stakes, joint ventures, development entities, or related-party operations can trigger exclusions that weren’t a problem when you were simpler.

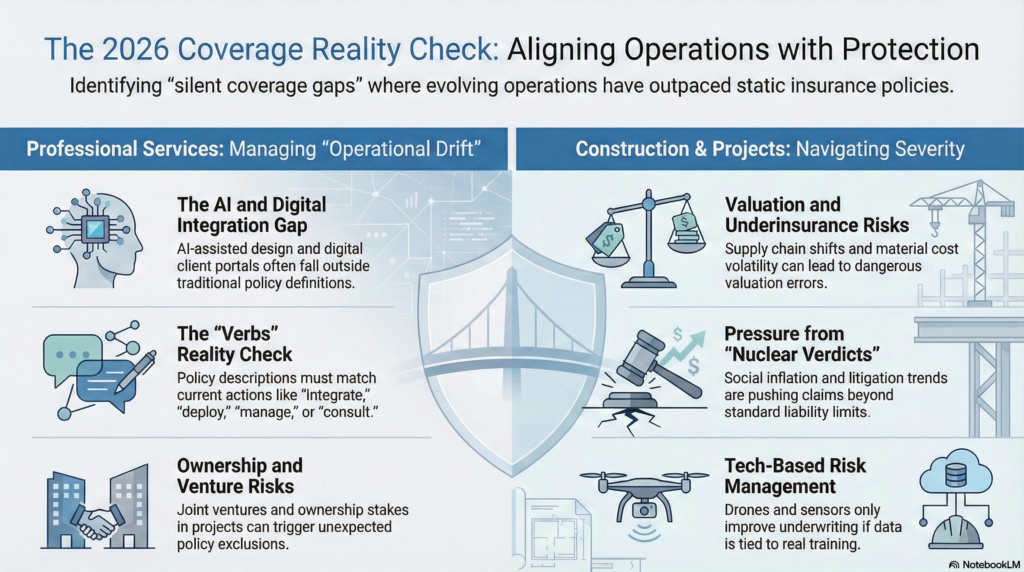

For professional firms: how do new service models change the risk?

Professional services are a clean example of operational drift—especially in law, accounting, architecture, and engineering—because the work is evolving faster than the insurance description.

In 2026, that drift often looks like:

- AI-assisted drafting, analysis, or design that becomes part of the deliverable

- Expanded advisory work (risk, compliance, owner’s rep, project management)

- Cross-state or multi-disciplinary work performed through partners or subcontractors

- Client portals and digital platforms used to exchange sensitive data

- Alternative fee arrangements and tighter contractual standards of care

Each can create a mismatch where a firm’s E&O assumptions don’t fully reflect the current delivery model, the contracts being signed, or the technology embedded in the workflow.

The prevention-first move is to map: scope of services + contract language/standard of care + data handling/client portal risk + third-party reliance (subs/partners) + AI usage, and make sure the insurance program matches the map.

For construction and project-driven businesses: what changes the risk profile in 2026?

Valuation and underinsurance

Material cost volatility and supply chain shifts can drive valuation errors. If property or builders risk values lag reality, claims can create large out-of-pocket gaps.

Litigation and severity

Large verdict trends can pressure liability and excess programs, especially when jobsite hazards or alleged faulty work causes third-party injury or property damage.

Technology-based risk management

Telematics, drones, sensors, and data-driven tools can improve safety and underwriting outcomes—but only if the data is used consistently and tied to real controls and training.

Key Takeaway

The goal isn’t more insurance. The goal is alignment—making sure your insurance description, exclusions, limits, and operational reality match before a claim tests them. A once-a-year coverage reality check – from someone you trust – is a simple prevention-first habit that can eliminate the most expensive surprises.

FAQ

What is a “silent coverage gap”?

It’s a mismatch where your business is doing something real (new service, tech-enabled process, ownership structure), but your policy wording or exclusions don’t match—so coverage may be limited when a claim happens.

How often should we review our insurance program if we’re growing?

At least annually, and anytime you add a new revenue stream, launch a tech platform, change ownership/financing, expand facilities, or take on new contractual risk. More importantly, consistent contact with your insurance broker allows for adjustments in real time that you might not consider an insurance issue.

Why are construction liability programs under pressure?

Severity trends like social inflation and large jury verdicts can push claims beyond standard limits, especially from third-party funded litigation or alleged faulty work.

What’s one sign our professional liability policy might be outdated?

If the policy’s definition of your services doesn’t match how you get paid today—or if you’ve added tech-enabled services, ownership stakes, or new operational verbs.

Does adding digital tools change professional liability needs?

Often, yes. There are various Professional Liability or Errors & Omissions policy forms – technology based services may be excluded from your traditional policies.