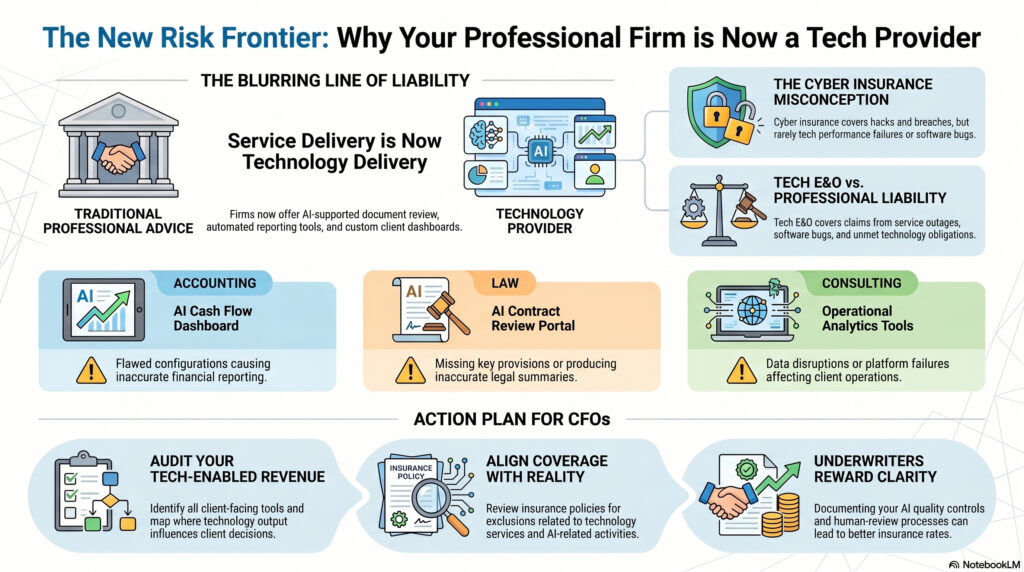

Technology risk is no longer limited to software companies.

Law firms, accounting firms, consultants, marketing firms, financial advisors, engineering firms, and other professional services businesses are increasingly using technology as part of their core service delivery. Some are using AI to analyze documents, generate work product, automate client communications, review contracts, summarize financial data, support tax workflows, build client dashboards, or deliver technology-enabled advisory services.

“A professional firm may still think of itself as a professional services firm. But from an insurance and contract perspective, it may now have exposures that look more like a technology provider.”

That creates an important question for CFOs: At what point does a professional services firm begin to carry technology company risk?

The Line Between Professional Service and Technology Service Is Blurring

Historically, a law firm provided legal advice, an accounting firm provided tax and financial services, and a marketing firm provided creative strategy. Technology supported the service, but it was not necessarily the service itself.

That is changing.

A professional firm may now offer:

- Client portals

- Automated reporting tools

- AI-supported document review

- Compliance dashboards

- Data analytics

- Custom workflow tools

- Software integrations

- Managed technology platforms

- AI-generated deliverables

- Subscription-based advisory portals

When technology becomes part of the client deliverable, the risk profile changes.

The firm may still think of itself as a professional services firm. But from an insurance and contract perspective, it may now have exposures that look more like a technology provider.

Why Cyber Insurance May Not Be Enough

Cyber insurance is designed to address certain losses from data breaches, ransomware, privacy events, funds transfer fraud, and related cyber incidents.

But what happens if the issue is not a hack?

What if an AI-supported tool produces incorrect output? What if a client dashboard fails? What if a software integration disrupts client operations? What if the firm offers a technology-enabled service that does not perform as promised? What if a client alleges financial harm because the firm’s platform, workflow, or automated process failed?

Those claims may not fit neatly into a cyber policy.

Tech errors and omissions insurance is designed to address claims arising from mistakes, oversights, failures, software bugs, service outages, data mishandling, inaccurate advice, missed deadlines, misrepresentation, and unmet technology obligations.

Professional Liability vs. Tech E&O

Professional liability insurance generally addresses claims related to the firm’s professional services. Tech E&O addresses claims tied to technology products or technology services.

The problem is that modern professional services may involve both.

Consider a few examples:

Accounting Firm Example: An accounting firm offers clients an AI-supported cash flow dashboard. The dashboard pulls financial data from multiple systems and produces projections. If a system error or flawed configuration causes inaccurate reporting and a client makes a poor financial decision, is that an accounting E&O claim, a technology E&O claim, or both?

Law Firm Example: A law firm offers clients an AI-supported contract review portal. If the tool misses a key provision or produces an inaccurate summary that contributes to a business loss, the exposure may extend beyond traditional legal malpractice concerns.

Consulting Firm Example: A consulting firm builds a client-facing operational analytics tool as part of its advisory service. If the tool fails, produces bad data, or disrupts the client’s operations, the firm may face allegations tied to technology performance.

Marketing Firm Example: A marketing agency provides technology-enabled campaign automation, data analytics, and customer segmentation. If a platform configuration error exposes client data or causes a failed campaign launch, multiple policies may need to be reviewed.

Why This Matters to CFOs

CFOs should care because technology-enabled services can change:

- Contract obligations

- Client indemnity requirements

- Insurance requirements

- Professional liability exposure

- Cyber exposure

- Intellectual property risk

- Data handling obligations

- Underwriting questions

- Claim complexity

The business may also be signing contracts that assume the firm has technology coverage, even if its insurance program has not evolved.

The issue is not only whether a policy exists. The issue is whether the coverage matches the way the business actually generates revenue.

What CFOs Should Do Next

A practical review should include:

- Identifying all client-facing technology tools

- Reviewing AI use in core service delivery

- Mapping where technology output influences client decisions

- Reviewing contracts for technology obligations, warranties, indemnity, and service-level commitments

- Comparing professional liability, cyber, and Tech E&O policies

- Reviewing exclusions for technology services, cyber events, contractual liability, and AI-related activities

- Documenting quality control, human review, testing, and approval procedures

- Ensuring employees understand when AI can and cannot be used

If a firm uses AI or technology in client work, it should be able to show how outputs are reviewed, validated, approved, and corrected. This provides underwriting clarity and helps us fit the right coverage language into your policies.

Underwriters Reward Clarity

Underwriters do not like ambiguity.

A firm that can clearly explain its services, technology tools, AI controls, data practices, contracts, and quality assurance process is in a stronger position than a firm that says, “We use some AI tools, but nothing major.”

The goal is to de-average from the competition. Businesses that can prove they manage risk well are easier to underwrite, easier to differentiate, and often positioned for lower costs during renewal.

Conclusion

Professional services firms may not think of themselves as technology companies. But if they are using AI, automation, client portals, analytics tools, or software-enabled deliverables as part of their client services, they may have technology company risk.

For CFOs, the key is to move from confusion to clarity. Identify where technology is part of the value proposition, determine how that changes the risk profile, and align insurance coverage with the actual services being delivered.

Stillwell Risk Partners helps professional services firms evaluate emerging technology risks, review coverage gaps, and build prevention-first strategies that protect revenue, reputation, and long-term insurability.

Does your policy exclude technology services? Book your complementary coverage review here.