When a liability claim occurs, many business leaders assume the insurance company decides whether to settle.

Sometimes that’s true. Sometimes it isn’t.

Certain liability policies, especially professional liability policies, may include a consent to settle clause. This provision can give the insured a voice in whether a claim is settled. That can be valuable, but it can also create financial trade-offs that CFOs need to understand before a claim occurs.

What Is a Consent to Settle Clause?

A consent to settle clause generally requires the insurer to obtain the insured’s approval before settling a claim.

If the insurer recommends accepting a settlement, the business usually has two choices:

- Accept the settlement recommendation.

- Reject the recommendation and continue defending the claim.

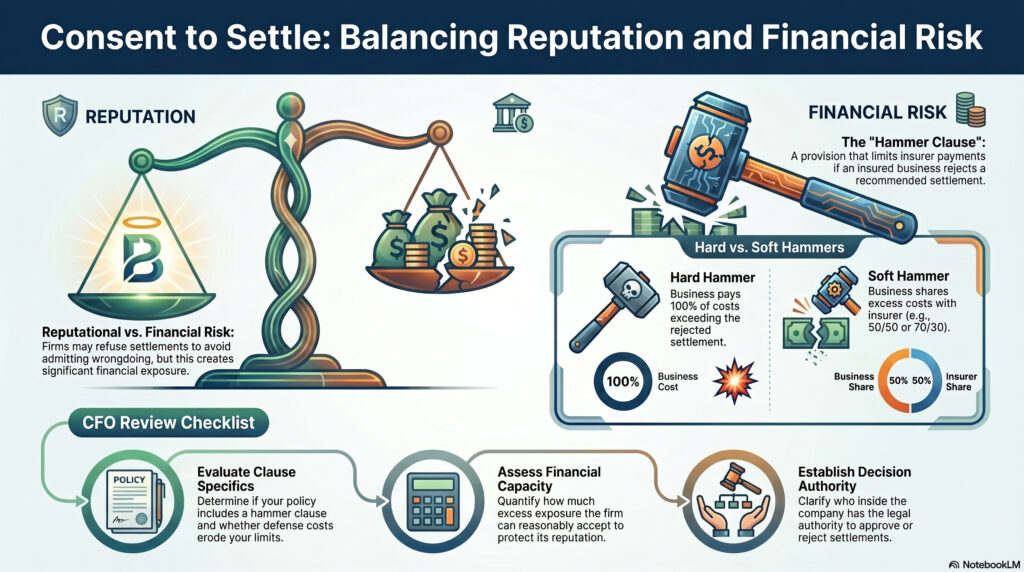

That sounds simple, but the financial consequences can be significant. Some policies include a hammer clause, which may limit how much the insurer will pay if the insured rejects a recommended settlement.

Why This Matters to CFOs

For many professional firms, a settlement is not just a financial transaction. It may create reputational consequences.

A law firm, accounting firm, consulting firm, healthcare organization, design firm, engineering firm, or contractor may not want to settle a claim if doing so implies wrongdoing or undermines client trust.

Without consent rights, the insurer may have broader discretion to resolve the claim based on cost efficiency. From the insurer’s perspective, settlement may be practical. From the business’s perspective, the reputational impact may be more complicated.

That is why this clause matters.

The Hammer Clause Problem

A hammer clause changes the decision.

If the insurer recommends settling for a certain amount and the insured refuses, the policy may cap the insurer’s obligation at the amount for which the claim could have been settled. The insured may then be responsible for additional defense costs, judgments, or settlements above that amount.

Some hammer clauses are hard. Others are soft.

“These provisions should be understood during policy review, not discovered during litigation.”

A hard hammer clause may sharply limit the insurer’s responsibility after settlement is rejected. A soft hammer clause may split additional costs between the insurer and insured using a coinsurance formula, such as 50/50, 70/30, or 80/20.

For CFOs, this creates a need to consider risk appetite and capacity: How much financial exposure is the company willing to retain in order to continue defending its reputation? How much exposure is the firm able to reasonably accept?

What CFOs Should Review

Before a claim occurs, CFOs should understand:

- Does the policy include a consent to settle clause?

- Does the policy include a hammer clause?

- Is the hammer clause hard or soft?

- What costs could shift back to the insured after rejecting settlement?

- Do defense costs erode the policy limit?

- How important is reputation in the company’s client acquisition and retention model?

- Who inside the company has authority to make settlement decisions?

- Has legal counsel reviewed the clause?

This is where going from confusion to clarity is accomplished. These provisions should be understood during policy review, not discovered during litigation.

How This Fits Into a Broader Risk Strategy

Insurance should be part of a broader risk strategy.

A business can reduce professional liability risk through strong contracts, clear scopes of work, documented client approvals, quality control, internal review procedures, and dispute escalation processes.

The consent to settle clause only matters after a claim exists. Prevention-first risk management reduces the chance that the business gets there in the first place.

Conclusion

Consent to settle provisions can be valuable, especially for businesses where reputation is central to long-term value. But these clauses can also shift financial risk back to the company if not understood clearly.

For CFOs, the key is to evaluate policy language before there is a claim and align coverage terms with the company’s risk tolerance, reputation strategy, and financial capacity.

Stillwell Risk Partners helps businesses review liability coverage, understand key policy provisions, and build prevention-first strategies that protect both balance sheet and reputation.

Not sure where to find these coverage provisions in your policy? Book your complementary coverage review here.